Battery Chemicals in Europe: Which Raw Materials Will Be Most Critical by 2030?

Europe's electric vehicle and energy storage ambitions are running headlong into a hard physical constraint: the raw materials needed to make modern batteries. Lithium, nickel, cobalt, manganese, and graphite form the backbone of today's lithium-ion cells, and every one of them is facing a steep demand curve as automakers electrify their fleets and grid-scale storage scales up. The question for European policymakers, manufacturers, and investors isn't whether demand will rise — that's already baked in — but which materials will become genuine bottlenecks, and how exposed Europe is to each one.

This article walks through the raw materials likely to matter most for European battery chemistry through 2030, why they're under pressure, and what's being done about it.

The Scale of the Challenge

It's worth starting with just how dramatic the projected demand growth is. Cobalt demand is expected to grow ninefold, while nickel, manganese, graphite, and lithium are forecast to require twelve to fifteen times more resources by 2035 compared to 2025 figures. Even on a shorter horizon, lithium demand for batteries is expected to grow fivefold by 2030 and fourteenfold by 2040 compared to 2020 levels, with graphite and nickel close behind.

What makes this particularly tricky for Europe is the starting point. The continent has very little domestic mining capacity for any of these materials, and while EU policy has pushed hard for cell manufacturing capacity to be built locally, the upstream raw material and refining stages remain dominated by a handful of countries outside Europe. McKinsey's analysis points to specific geographic concentrations: Indonesia for nickel, the Democratic Republic of Congo for cobalt, and Argentina, Bolivia, and Chile for lithium. Refining capacity is even more concentrated, with China holding a dominant position across nearly the entire battery materials value chain.

Against that backdrop, here's how the major raw materials stack up.

Lithium: The Material Everyone's Watching

If there's one element that has come to symbolize the battery materials challenge, it's lithium. The reason is straightforward: lithium-ion battery production already consumes the vast majority of global lithium reserves, a share projected to rise to roughly 95% by 2030. Unlike nickel or cobalt, lithium doesn't have a large existing industrial market to fall back on or divert from — battery demand essentially is the lithium market now.

The supply side is improving, but not fast enough by most estimates. Looking ahead to a scenario consistent with climate goals, expected supply from existing mines and projects under construction is estimated to meet only about half of projected lithium and cobalt requirements by 2030. Newer extraction techniques — particularly direct lithium extraction (DLE) from brines, which is faster and less land-intensive than traditional evaporation ponds — are seen as part of the solution, but these technologies are still progressing while demand continues to outpace supply.

For Europe specifically, this is a double-edged situation. On one hand, the continent has identified lithium deposits of its own — in Portugal, Germany (notably the geothermal brine projects in the Upper Rhine Valley), the Czech Republic, Serbia, and Finland — and several projects are working toward production this decade. On the other hand, even optimistic European production scenarios would cover only a fraction of projected EU demand, meaning lithium imports (and lithium chemical processing capacity, which is currently almost entirely located in China) will remain a strategic vulnerability well past 2030.

Nickel: A Tighter Squeeze Than It Looks

Nickel often gets less attention than lithium in public discussion, partly because nickel has a long history as an industrial metal used in stainless steel, and global nickel production is large in absolute terms. But the nickel that matters for batteries — high-purity, "Class 1" nickel suitable for battery-grade precursors — is a much smaller and more constrained category.

Fears of a nickel shortage driven by the shift to battery electric vehicles have already triggered significant new mining investment, particularly in Southeast Asia, though even more supply will be needed, and McKinsey's report suggests the possibility of a slight shortage by 2030 as battery makers compete with the steel industry for the same Class 1 material. The supply-demand balance for battery-grade nickel was already projected to tighten by the end of the decade: the global supply and demand balance for nickel is expected to become tight by around 2029.

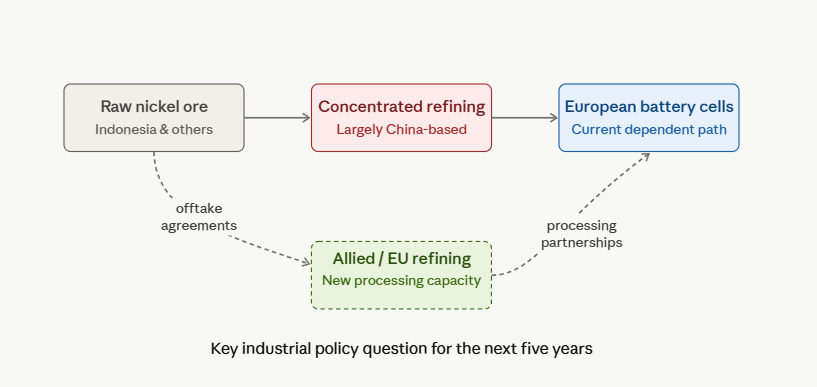

Indonesia's dominance in nickel processing is the key geopolitical fact here. The country has rapidly expanded its nickel processing industry, much of it through Chinese investment, and has become the central node for converting raw nickel ore into the chemical forms batteries require. For Europe, securing offtake agreements and processing partnerships outside this concentrated supply chain — including potential European or allied refining capacity — is likely to be one of the more consequential industrial policy questions of the next five years.

Cobalt: Falling Share, Rising Volume

Cobalt presents an interesting paradox. Battery chemistry trends are actively moving away from cobalt — high-nickel NMC formulations (like NMC 811, with 80% nickel and only 10% cobalt) and cobalt-free lithium iron phosphate (LFP) chemistries are both gaining market share specifically because cobalt is expensive, ethically fraught (given its concentration in artisanal mining operations in the DRC), and supply-constrained.

Yet even with its declining share of battery chemistry, absolute cobalt demand is still expected to climb. While cobalt's share in the battery chemistry mix is expected to decrease, absolute demand for cobalt across all applications could still rise by about 7.5% per year between 2023 and 2030, and McKinsey's broader analysis described shortages as unlikely but flagged ongoing structural concerns. Other longer-range projections paint an even starker picture of cumulative growth, with cobalt demand expected to grow ninefold by 2035 compared to 2025.

The DRC's near-monopoly on cobalt mining (it accounts for the large majority of global supply) means that, regardless of chemistry trends, cobalt remains a single-point-of-failure risk for any battery supply chain — including Europe's. This is one of the strongest arguments for the chemistry shift toward LFP and other cobalt-free chemistries that's already underway in the European market, even though LFP currently lags NMC in energy density.

Graphite: The Quiet Bottleneck

Graphite doesn't generate the same headlines as lithium or cobalt, but it's arguably one of the most concentrated and least diversified parts of the battery supply chain. Both natural and synthetic graphite are used for the anode in virtually all lithium-ion batteries, and the processing of graphite into battery-grade material — a process involving purification and spheroidization — is overwhelmingly dominated by China.

The global supply and demand balance for graphite was already expected to become tight by around 2024, reflecting how quickly this material moved from a non-issue to a pressure point. At the same time, demand for graphite is projected to increase by roughly 19 times by 2040 compared to 2020 levels — one of the steepest growth curves of any battery material.

For Europe, graphite represents a particularly acute exposure because there is essentially no European synthetic graphite production at scale, and natural graphite mining in Europe (with some prospects in Sweden, Norway, and elsewhere) remains nascent. Several European battery gigafactories have signed offtake agreements with graphite producers in North America and elsewhere specifically to diversify away from Chinese-processed material, but building out independent anode material processing capacity in Europe is likely to take most of this decade.

Manganese: Underestimated, but Not Trivial

Manganese is often treated as the "easy" material in the battery raw materials conversation — it's geologically abundant and widely mined for the steel industry. But battery-grade manganese requires conversion into high-purity manganese sulfate monohydrate (HPMSM), and this refining step turns out to be surprisingly difficult.

Despite manganese being plentiful in raw form, refining it into the high-purity manganese sulphate monohydrate needed for batteries is complex and requires stringent control to eliminate impurities, and production growth projections for HPMSM remain conservative relative to anticipated demand by 2030. On top of that, the global manganese supply and demand balance was projected to become tight as early as 2025 — making it one of the earliest bottlenecks to bite, even if it's less discussed than lithium or nickel.

For Europe, manganese is a case where the raw material itself isn't the problem — it's the refining capacity. This is arguably good news in one sense: building HPMSM processing capacity is a more tractable industrial challenge than developing entirely new mines, and several European and allied projects have been announced to address exactly this gap.

How Much Will Recycling and New Chemistries Help?

Two structural trends could meaningfully ease pressure on these materials over the medium term, though their impact through 2030 specifically is likely to be limited.

Recycling and second-life batteries are often cited as a long-term solution, but the timing matters. Recycling and second-life applications are expected to have only a limited impact during the early 2030s, with their contribution surging in subsequent decades — particularly in unlocking nickel and cobalt currently locked in discarded batteries. Looking further out, recycling could contribute up to 51% of EU cobalt demand and 42% of EU nickel demand by 2040 — substantial figures, but on a timeline well beyond 2030. Simply put: there aren't yet enough end-of-life batteries in the system for recycling to be a major supply source this decade, though the regulatory groundwork (including EU rules on minimum recycled content) is being laid now.

Alternative chemistries are moving faster. Sodium-ion batteries, which use more abundant and geographically diversified materials, are emerging as an alternative to lithium-ion systems, though they remain at an earlier stage of commercialization and typically offer lower energy density. More immediately impactful is the continued shift toward LFP and LFP-variant chemistries, which several analyses note could help reduce reliance on scarce materials like cobalt and nickel through encouraging research and development in alternative battery chemistries such as LFP, LMFP, and sodium-ion, alongside advances in solid-state batteries and structural battery integration.

What This Means for Europe Through 2030

Putting it all together, a rough hierarchy of criticality for Europe through 2030 looks something like this:

Lithium sits at the top — not necessarily because Europe can't access it, but because the chemical processing of lithium into battery-grade material is so concentrated outside Europe, and because demand growth is so steep that even modest supply shortfalls translate into price volatility. Graphite is close behind, given the near-total absence of European processing capacity and the early onset of supply tightness. Nickel and manganese represent more of a "refining gap" than a raw material gap — the ores exist, but battery-grade processing capacity needs to be built rapidly. Cobalt remains a geopolitical risk concentrated in a single country, even as its role in battery chemistry gradually shrinks.

For European industrial strategy, the throughline across all five materials is the same: mining is necessary but not sufficient. The chokepoint, in nearly every case, is mid-stream chemical processing and refining — precisely the stage where China currently holds an outsized position. Even as global production becomes more diversified, China is expected to remain the major supplier of battery-grade raw materials through 2030.

Whether Europe can meaningfully shift this balance by the end of the decade will depend less on discovering new deposits and more on whether the continent can build — quickly, and at scale — the unglamorous but essential refining and chemical conversion plants that turn raw ore into battery-ready chemicals. The race for battery materials in Europe, in other words, isn't really a mining race. It's a chemistry race.