China's Phosphate Export Restrictions: What European Buyers Should Prepare For

The global phosphate market has been quietly rewiring itself since 2021, and for European chemical buyers, the implications are now impossible to ignore. China is historically the world’s largest phosphate producer and a dominant exporter, and has been systematically tightening its grip on outbound shipments. What began as a series of quota adjustments has evolved into something far more structural: a strategic reorientation of Chinese phosphate policy that may define global supply conditions well into the next decade.

For procurement teams sourcing diammonium phosphate (DAP), monoammonium phosphate (MAP), phosphoric acid, or phosphate rock for industrial and agricultural applications, understanding what is driving this shift (and what to do about it) is no longer optional.

How We Got Here: A Decade of Tightening

China’s relationship with phosphate exports has never been simple. The country holds roughly 5% of the world's phosphate reserves but has long accounted for over 40% of global production, a discrepancy that policymakers in Beijing have watched with growing unease. Since 2016, annual phosphate mining has been capped at 150 million metric tons, a quota that has since been tightened further as authorities seek to protect what they increasingly classify as a strategic and non-renewable national resource.

Formal export restrictions began in spring 2021, introduced as a measure to prioritize domestic availability and keep food inflation in check. At the time, few expected these measures to persist; China had previously cycled through periods of export restriction and liberalization. However, this time, the restrictions have only become more stringent.

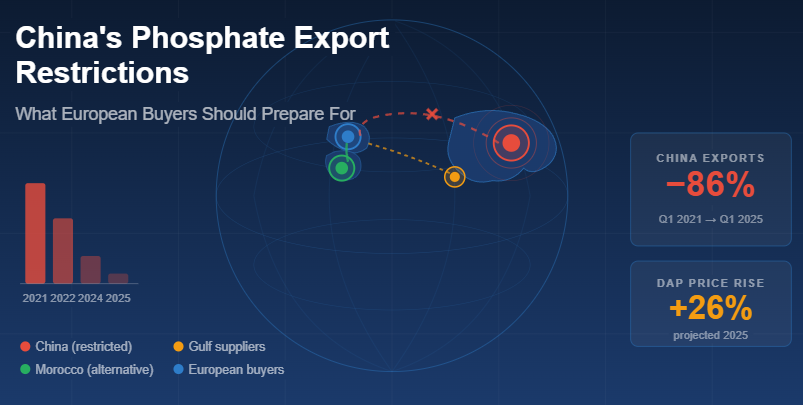

The numbers tell a stark story. In 2019 and 2020, China exported an average of nine million metric tons of ammoniated phosphates annually, reaching a record ten million metric tons in 2021. By 2024, that figure had collapsed to 6.6 million metric tons. And in the first quarter of 2025, Chinese exports of phosphate fertilizers amounted to just 111,000 metric tons - compared to a three-year average of 785,000 metric tons for the same period and over 1.5 million metric tons in Q1 2021. In March 2025 alone, China shipped only 13,000 metric tons of phosphate, against 950,000 in the same month three years prior.

In December 2025, the signals became even clearer: China’s phosphate fertilizer industry reached a broad consensus that no new export plans would be proactively scheduled before August 2026. While framed as a voluntary industry action rather than a government mandate, the meeting was held under the direction of the National Development and Reform Commission, making its binding character unmistakable to market observers.

What Is Driving the Restrictions?

Three structural forces are at work, and each deserves careful attention because none of them is likely to reverse quickly.

Resource conservation. With a reserve-to-production ratio of just 34 years — far below the global average of 308 — China has legitimate long-term concerns about phosphate depletion. High-grade ore is increasingly scarce, and environmental regulators have imposed stricter controls on mining operations. Industry consolidation has meant that leading enterprises like Yuntianhua and Chuanheng are increasingly diverting phosphate rock to their own downstream processing rather than selling it externally.

The electric vehicle sector. This is perhaps the most underappreciated driver. Each ton of lithium iron phosphate (LFP) — the battery chemistry powering the majority of Chinese EVs and a growing share of global energy storage systems — consumes approximately 3.5 tons of phosphate rock. By 2025, the new energy sector alone was projected to add 4.4 million additional tons of phosphate demand within China, accounting for over 4% of total domestic phosphate output. Chinese automobile production has accelerated in every month of 2025 compared to prior years. The demand from industry, in other words, is directly competing with export availability.

Cost and price dynamics. Sulfur — which accounts for 30–40% of phosphate fertilizer production costs — has experienced extraordinary price inflation, rising some 230% in 2024 alone. Domestically, average MAP prices reached approximately 3,600 yuan per ton in May 2025, a 30% year-on-year increase, while DAP was quoted at around 4,100 yuan per ton in December 2025, up 28%.

The Global Market Consequences

The ripple effects have been immediate and significant. DAP prices globally climbed from $568 per metric ton in December 2024 to $615 in March 2025, with actual transaction prices in some markets running even higher. In Northwest European markets, DAP CFR prices touched an average of $665 per metric ton in early 2025 as supply tightened. The World Bank has projected DAP prices to rise 26% across 2025 before any meaningful easing.

Critically, the gap left by China has not been filled. Five countries dominate phosphate exports globally — Morocco, Russia, China, the United States, and Saudi Arabia — and with China stepping back, analysts have noted plainly that the world simply does not have the excess production capacity to compensate for the volume differential. Russia and Saudi Arabia are already operating at maximum capacity, with new production not expected online until 2027 to 2028. Morocco has increased exports since 2022, but growth has been gradual and has been partially diverted toward triple superphosphate (TSP) rather than the more widely used DAP and MAP.

Europe’s Specific Vulnerability

European buyers face this disruption from a position of structural weakness that predates the current restrictions. The EU imports approximately 82% of its phosphate rock consumption, with the continent’s only operational mine — located in Finland — meeting just 5 to 10% of European agricultural demand. In 2024, EU companies purchased phosphorus fertilizers and phosphates worth nearly €4 billion from outside the Union.

Morocco is Europe’s largest single supplier, accounting for approximately €1.4 billion in phosphate imports in 2024. Russia remains the EU’s second-largest phosphate supplier despite the war in Ukraine, accounting for roughly 25% — close to €1 billion — of total EU phosphate imports in 2024. Fertilizers remain exempt from EU sanctions precisely because of the food security risk that cutting Russian supply would create, a political compromise that has effectively kept European buyers reliant on an uncomfortable source.

The EU’s Carbon Border Adjustment Mechanism (CBAM) adds a further complication. Since 2025, fertilizer exporters to the EU are required to submit verified carbon emissions reports, with financial penalties for non-compliance taking effect in 2026. This has already begun shifting European buyer preferences toward lower-carbon phosphate sources — particularly Moroccan and Jordanian product — while placing higher-carbon alternatives at a competitive disadvantage.

What European Buyers Should Be Doing Now

The situation calls for a deliberate, proactive procurement strategy rather than reactive purchasing. Several steps can meaningfully reduce exposure:

• Extend your procurement horizon. The days of placing short-term spot orders and relying on market availability are effectively over for phosphate. With inventories at historically low levels across key markets at the end of 2024 and no clear timeline for Chinese supply to normalize, buyers who wait until need arises will face both premium pricing and extended delivery uncertainty. Building six-to-twelve-month forward coverage — where cash flow allows — provides meaningful insulation.

• Audit your supplier concentration. If your phosphate supply chain runs primarily through a single geography or a small number of intermediaries, this is the moment to map and stress-test it. European buyers overly concentrated in Russian-origin material carry meaningful geopolitical risk, while those reliant on spot Moroccan availability without contracted volumes may find themselves competing with Indian, Brazilian, and Southeast Asian buyers for the same cargoes.

• Engage directly with Moroccan and Jordanian producers. OCP and Jordan Phosphate Mines Company (JPMC) are the two producers most positioned to grow their share of European supply in the medium term. Establishing direct purchasing relationships — rather than relying solely on trader intermediation — provides both preferential access and greater price transparency.

• Assess CBAM exposure across your supply chain. If you have not already mapped the carbon footprint of your phosphate inputs, the regulatory clock is running. Suppliers unable to provide verified emissions data will either exit the European market or pass compliance costs onto buyers. Building sourcing preference for compliant suppliers now avoids a more disruptive transition under deadline pressure in 2026.

• Invest in demand forecasting and inventory management. In a market characterized by price volatility and supply uncertainty, the ability to identify procurement windows and hold strategic inventory is a genuine competitive advantage. The spread between domestic Chinese prices and international prices reached 56.6% for MAP and 44.6% for DAP as of mid-2025 — figures that illustrate just how divorced global supply dynamics have become from Chinese production costs.

The Medium-Term Outlook

There is no credible scenario in which Chinese phosphate exports return to pre-restriction volumes in the near term. The EV battery demand trajectory is secular, not cyclical. Resource conservation policy reflects genuine long-run concerns about reserve depletion. And the December 2025 industry consensus — effectively suspending new export scheduling through August 2026 — suggests that even a modest reopening of the window is unlikely before mid-year at the earliest.

New supply capacity is coming, but slowly. Morocco’s ongoing expansion projects, Saudi Arabia’s Ma’aden complex, and additional capacity in Brazil are all expected to contribute meaningfully by 2027 and 2028. Until then, the structural tightness in the market is the baseline, not the exception.

For European industrial buyers of phosphates — whether for fertiliser, food-grade applications, detergents, water treatment, or flame retardants — the window to build supply resilience at reasonable cost is now. Prices are elevated but not at crisis levels. Supply is constrained but not yet critically disrupted for buyers who act deliberately. That balance may not hold.